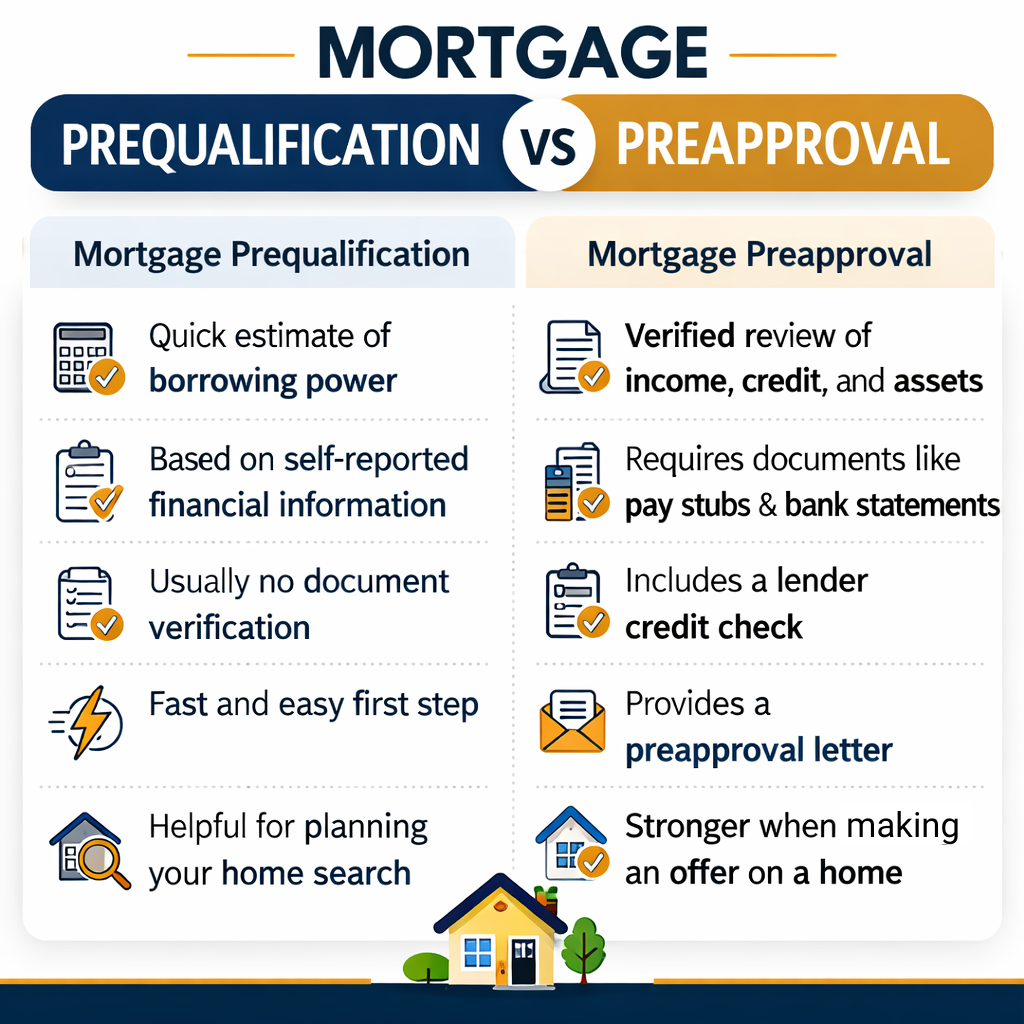

A mortgage preapproval is a more detailed and verified review of your finances. Instead of relying only on estimates, a lender reviews documentation such as income statements, employment history, credit reports, and asset information. The goal is to determine how much you are likely to qualify for based on verified financial data. My goal is to gather as much info up-front as I can and then submit for our first round of underwriting as quickly as possible. The path to a smooth closing is laid through early preparation!

Once the review is complete, the lender typically issues a preapproval letter. This letter confirms that your finances have been evaluated and that you appear qualified for a mortgage up to a certain amount, subject to final underwriting and property approval.

Why Preapproval Matters

Preapproval gives you a clearer picture of your buying power and strengthens your position when making offers. Real estate agents and sellers often prefer working with preapproved buyers because it shows that financing has already been reviewed by a lender.

This step can be especially valuable for military families relocating to the area through PCS orders. Buyers moving to communities near Kings Bay Naval Submarine Base often start touring homes soon after arriving, and having a preapproval letter ready can make the process far smoother when the right home appears.